Consumer-directed health plans have been useful in controlling the rise of health costs over the last several years, but the survival of these plans is threatened by the new health overhaul law.

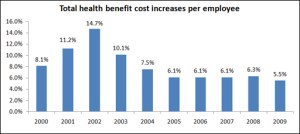

Mercer’s latest National Survey of Employer-Sponsored Health Plans found that major employers held total health benefit cost increases per employee to 5.5 percent in 2009 the lowest increase in a decade (see chart below). Participation in consumer-directed health plans, as well as health management programs, has been growing over the last few years as companies sought ways to successfully engage employees as partners in managing costs and care.

Source: Mercer’s National Survey of Employer-Sponsored Health Plans; Bureau of Labor Statistics, Consumer Price Index, U.S. City Average of Annual Inflation (April to April) 1990-2009; Bureau of Labor Statistics, Seasonally Adjusted Data from the Current Employment Statistics Survey (April to April) 1990-2009.

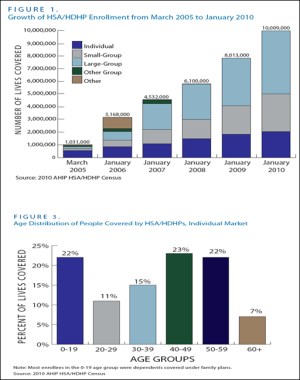

Enrollment in consumer-directed plans grew to an estimated 23 million people in 2009, up from 18 million people in 2008-a 27% increase, according to an April report by the American Association of Preferred Provider Organizations.

Among the most notable is the growing adoption of Health Savings Accounts. Ten million Americans now are covered by HSA-qualified health plans, up from eight million last year, according to the latest survey by America’s Health Insurance Plans. To open tax-free health savings accounts, people first must be enrolled in high-deductible health insurance plan.

Unfortunately, ObamaCare threatens to render these plans a thing of the past. Until now, employers have had the flexibility to tailor benefit and cost structures to fit their budgets and corporate cultures, but the new health overhaul law will limit their options in the future.

Under the new law, the Department of Health and Human Services will make the ultimate ruling on HSAs when it decides how to calculate the actuarial value of the high-deductible health insurance policies that must accompany health savings accounts.

The health law requires also that all insurance policies will be required to provide a minimum actuarial value of at least 60 percent for the benefits covered. If HHS allows contributions by individuals and employers to health savings accounts to “count” as part of the actuarial value, then HSAs and other account-based plans would likely meet the test. But if contributions are not included, the plans likely would not qualify, removing an important tool to hold health costs down.

HSAs couple a tax-favored savings account used to pay medical expenses with a high-deductible health plan that meets certain requirements for deductibles and out-of-pocket expense limits. Most cover preventive care services, such as routine medical exams, immunizations and well-baby visits, without requiring enrollees to first meet the deductible. The funds in the HSA are deposited tax free, interest earned is tax free, and the account is owned by the individual and may be rolled over from year to year.

The new AHIP study underscores the value of consumer-directed plans in achieving key goals of the health reform effort. Here are some highlights of the AHIP survey of people enrolled in HSA-qualified health insurance:

- Lower premiums: Monthly premiums for individuals aged 30 to 54 averaged $2,465 a year ($205 a month) and $5,335 for a family ($445 a month) less than half the average costs of traditional plans.

- Larger companies: The fastest growing market for HSA/HDHP products was large-group coverage, which rose by one-third, followed by small-group coverage, which grew by 22 percent.

- PPOs preferred: Overall, preferred provider organizations (PPOs) were the most popular insurance type, with 88 percent of enrollees. They generally have access to negotiated discount arrangements with health care professionals when paying bills from their HSA accounts.

- More consumer information: More than 90 percent of responding companies reported offering access to HSA account information, health education information, physician-specific information, and personal health records as consumer decision support tools for their members.

- Not just for the young: Fifty-two percent of all individual market enrollees — including dependents covered under family plans — were aged 40 or older so they clearly are not just for the young, as critics claim.

The charts below tell the story of success:

Indiana Gov. Mitch Daniels, a Republican, says providing the HSA option to state employees will save the state at least $20 million this year, and employees will save $8 million compared to their coworkers in traditional health plans. More than 70% of Indiana’s 30,000 state employees have selected the HSA option.

Gov. Daniels says that employees become more active participants in their health care, making smarter and more cost-effective decisions visiting hospital emergency rooms 67% less often and using generic drugs more than those in conventional plans, for example. An independent survey by Mercer found no evidence that HSA members are deferring needed treatment or preventive care.

Many companies, such as Whole Foods, offer another form of CDHC plan called Health Reimbursement Arrangements. HRAs give employers more flexibility in shaping their health benefit packages, including the ability to offer account-based plans and provide incentives for prevention and wellness activities. But, unlike HSAs, HRA account balances generally are not portable after employees leave the company.

Both products are helping to make health insurance more affordable and are helping companies to lower health costs.

Competition works when consumers are engaged in getting better value for their health care dollars. Policymakers would be well-advised to make sure that these consumer-friendly plans remain as an option for both individuals and employers so they can continue to have these tools to engage employees as partners in managing health costs.

Grace-Marie Turner is president of the Galen Institute, www.galen.org, a non-profit research organization focusing on patient-centered health reform initiatives. She can be reached at gracemarie@galen.org.