If the Supreme Court does rule the individual mandate unconstitutional will it really bring down the whole law?

I don’t see it.

First, the individual mandate isn’t even close to what it has been made to be — a provision that would protect the integrity of the health insurance market by forcing people to buy health insurance before they became sick. At best, it’s a tepid attempt at that.

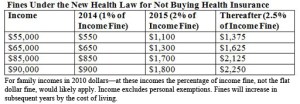

The individual mandate’s fine for not buying coverage is 1 percent of family income or $95 for each family member not covered, whichever is greater in 2014; 2 percent of income or $325 per family member, whichever is greater in 2015; and $695 or 2.5 percent of income or whichever is greater in subsequent years (kids are half price!).

These are meaningful fines for not buying insurance, but only a fraction of what a consumer would pay for health insurance.

Here’s how the individual mandate’s fine for non-compliance actually works for a number of representative family income levels based upon 2010 incomes and poverty levels:

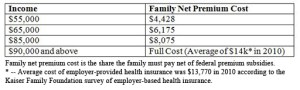

Alternatively, here is what families would be required to pay under the health law toward their health insurance premiums based upon their total family income — net of the federal subsidy — in 2010 dollars:

So, under the health law’s individual mandate, this $55,000 family would likely pay no more than $550 in fines the first year, $1,100 the second year and $1,375 in fines the third and subsequent years; or, alternatively, have to pay $4,428 for insurance net of the federal subsidy in the exchange.

A family making $85,000 a year (400 percent of poverty) would have to pay $8,075 for their share of the cost of health insurance in the exchange or likely pay a fine in the first year of $850 that would likely cap out at 2.5 percent of $88,000, or $2,125, in later years.

Families would also have to pay their share of deductibles and co-pays within the insurance policies they purchased.

The fine families would pay for ignoring the individual mandate to purchase health insurance is significant but only a fraction of what the insurance would cost.

If the individual mandate is eventually held unconstitutional by the Supreme Court there will be attempts to substitute an alternative means to protect the insurance market from the “anti-selection” that would occur as people held back on purchasing health insurance until they needed it.

One possible alternative to the individual mandate would be to allow consumers to purchase coverage only at limited open enrollment periods — buy it now or you won’t be able to get it when you get sick.

Given how tepid the current individual mandate penalties are, such an alternative scheme could be much more effective in protecting the insurance markets, as well as far more politically palatable for consumers faced with paying either an unaffordable insurance fine or an even more unaffordable insurance premium, than the current weak individual mandate before the courts.

All of the focus on the recent Richmond federal court ruling misses the big picture on health insurance affordability under the new law: Many middle class families will not be happy with or be able to afford the fines nor will they be able to afford the much higher cost of health insurance — even after the federal subsidy.